pymc.Pareto#

- class pymc.Pareto(name, *args, rng=None, dims=None, initval=None, observed=None, total_size=None, transform=UNSET, default_transform=UNSET, **kwargs)[source]#

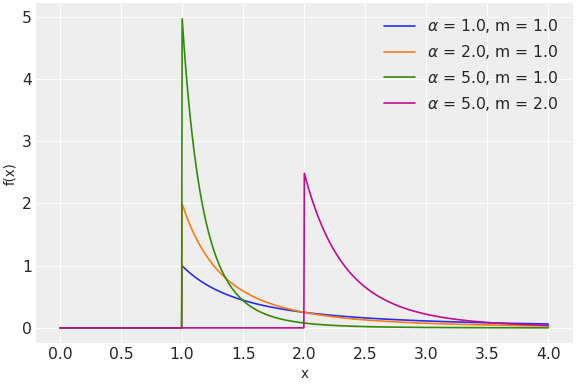

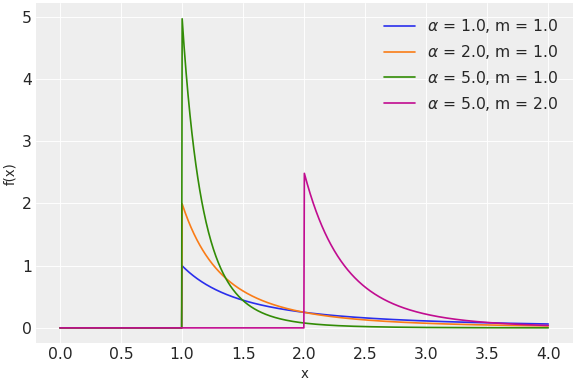

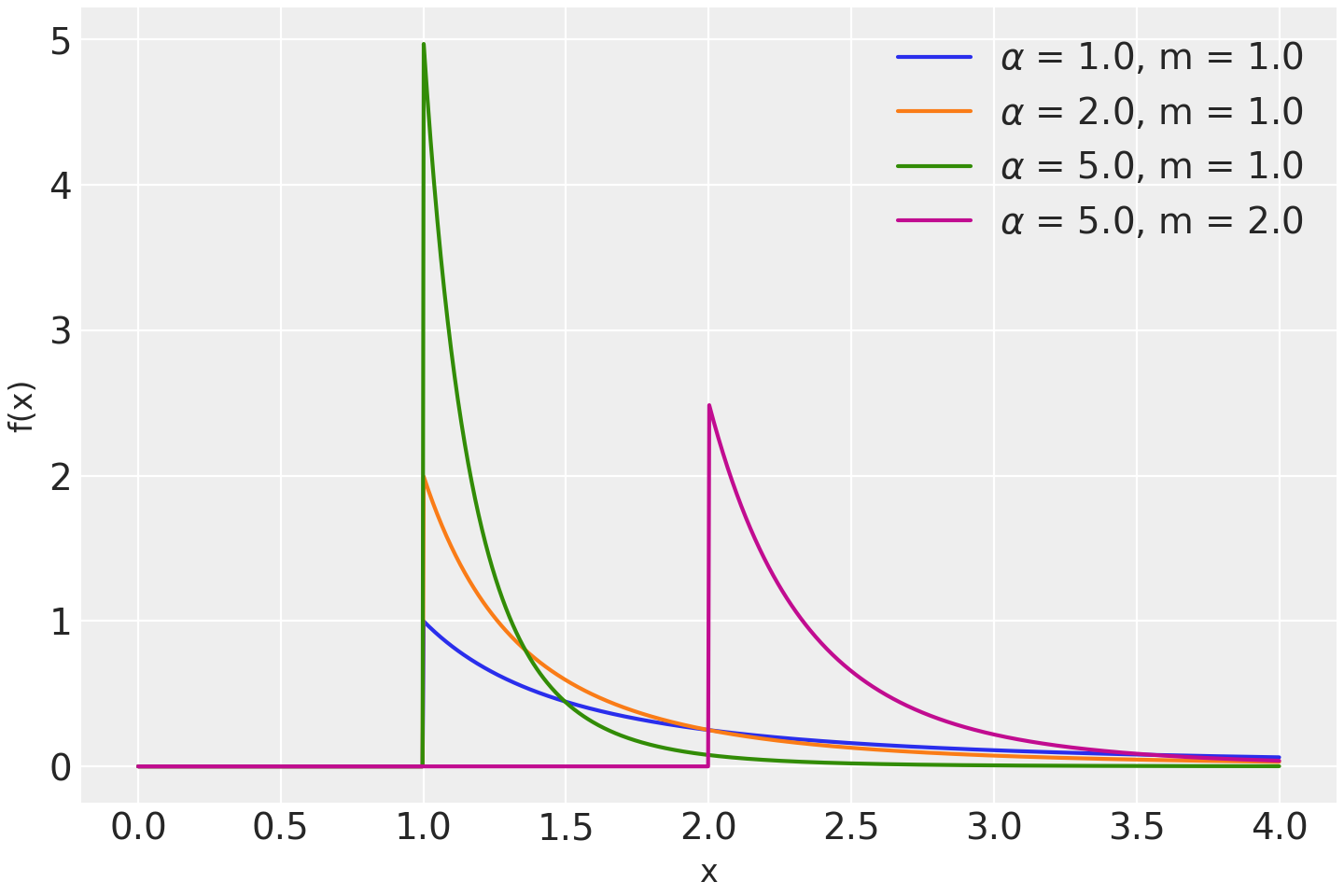

Pareto distribution.

Often used to characterize wealth distribution, or other examples of the 80/20 rule.

The pdf of this distribution is

\[f(x \mid \alpha, m) = \frac{\alpha m^{\alpha}}{x^{\alpha+1}}\](

Source code,png,hires.png,pdf)

Support

\(x \in [m, \infty)\)

Mean

\(\dfrac{\alpha m}{\alpha - 1}\) for \(\alpha \ge 1\)

Variance

\(\dfrac{m \alpha}{(\alpha - 1)^2 (\alpha - 2)}\) for \(\alpha > 2\)

- Parameters:

- alphatensor_like of

float Shape parameter (alpha > 0).

- mtensor_like of

float Scale parameter (m > 0).

- alphatensor_like of

Methods

Pareto.dist(alpha, m, **kwargs)Create a tensor variable corresponding to the cls distribution.

{kind=link}

{kind=link}