Hidden Markov Models in PyMC: marginalize and recover a DiscreteMarkovChain#

A hidden Markov model (HMM) describes a system that moves through a sequence of hidden discrete states, where each state emits a noisy observation. We never see the states directly; we only see the emissions, and we want to reason backward to the states that most likely produced them.

This notebook works through a tiny weather example: the hidden state is whether a day is rainy or sunny, the weather is “sticky” (it tends to persist from one day to the next), and our only measurement is a noisy thermometer. From the temperatures alone we will recover the most likely sequence of hidden weather states, together with our uncertainty about it.

The classic HMM inference questions are the evidence (how likely is the observed data), filtering and smoothing (the posterior over hidden states given the data), and decoding (the single most likely state path). This notebook focuses on the smoothing posterior, obtained through two composable tools from pymc_extras. For a general introduction to automatic marginalization of discrete variables, see Automatic marginalization of discrete variables.

This example showcases three additions that together make HMM inference in PyMC turnkey:

Time-varying transition matrices.

DiscreteMarkovChainacceptstime_varying_P=True, soPcan carry one transition matrix per step with shape(*batch, steps, k, k).Marginalization of a whole chain.

marginalizecan integrate aDiscreteMarkovChainout of a model analytically (the forward algorithm), leaving only continuous parameters for NUTS to sample.Recovery of the hidden states.

recover(and the lower-levelconditional) can reconstruct the posterior over a marginalizedDiscreteMarkovChain. The trick that makes this work is that the conditional posterior of the chain is itself a time-inhomogeneousDiscreteMarkovChain, which is exactly why the time-varyingPsupport from point 1 is needed.

Prepare Notebook#

import arviz as az

import matplotlib.pyplot as plt

import numpy as np

import pymc as pm

from pymc_extras.distributions import DiscreteMarkovChain

from pymc_extras.marginal import conditional, marginalize, recover

%config InlineBackend.figure_format = 'retina'

az.style.use("arviz-darkgrid")

plt.rcParams["figure.figsize"] = [10, 6]

plt.rcParams["figure.dpi"] = 100

plt.rcParams["figure.facecolor"] = "white"

rng = np.random.default_rng(42)

Why hidden discrete states are hard#

PyMC’s default sampler is NUTS, a gradient-based method. Gradients only exist for continuous parameters, so NUTS cannot move a discrete latent variable such as our per-day weather state. Historically this left a few options: sample the discrete states with a bespoke Gibbs or Metropolis step (which mixes slowly and couples awkwardly to the continuous parameters), or hand-write the forward-backward recursions for the specific model at hand.

Marginalization offers a cleaner path. Because the hidden states are discrete and finite, we can sum them out of the likelihood exactly. NUTS then samples only the smooth, continuous parameters (here the observation noise), and we reconstruct the hidden states afterward from their exact conditional posterior. The two steps below, marginalize and recover, automate exactly this.

The weather and the thermometer#

We describe eight days of weather with a single generative model and draw one realization from it. The hidden state is 0 for rain and 1 for sun, and the weather is sticky: each day it stays the same with probability 0.9. The thermometer reads about 0 degrees Celsius on rainy days and about 20 degrees on sunny days, corrupted by Gaussian noise with standard deviation true_sigma.

Rather than writing the data-generating process by hand and then again as a PyMC model, we build the model once, clamp sigma to its true value with pm.do, and take a single prior draw. This gives us both the hidden weather path (true_sunny_day) and the observed temperatures (obs_temp) from one source of truth.

# Hidden weather: 0 = Rain, 1 = Sun. Weather is "sticky": it tends to persist.

P = np.array(

[

[0.9, 0.1], # Rain -> [Rain, Sun]

[0.1, 0.9], # Sun -> [Rain, Sun]

]

)

n = 8

days = np.arange(n)

true_sigma = 4.0

# A single generative model: a sticky Markov chain over the hidden weather with a

# noisy thermometer emission. We reuse this exact model for inference below.

with pm.Model(coords={"day": days}) as generative_model:

sigma = pm.HalfNormal("sigma", 5.0)

init = pm.Categorical.dist(p=[0.5, 0.5]) # day-1 prior: 50/50

sunny_day = DiscreteMarkovChain("sunny_day", P=P, init_dist=init, dims="day")

pm.Normal("temp", mu=sunny_day * 20.0, sigma=sigma, dims="day")

# Draw a single realization with the observation noise clamped to a known value.

prior_draw = pm.sample_prior_predictive(

model=pm.do(generative_model, {"sigma": true_sigma}),

draws=1,

var_names=["sunny_day", "temp"],

random_seed=156,

)

true_sunny_day = prior_draw.prior["sunny_day"].sel(chain=0, draw=0).to_numpy()

obs_temp = prior_draw.prior["temp"].sel(chain=0, draw=0).to_numpy()

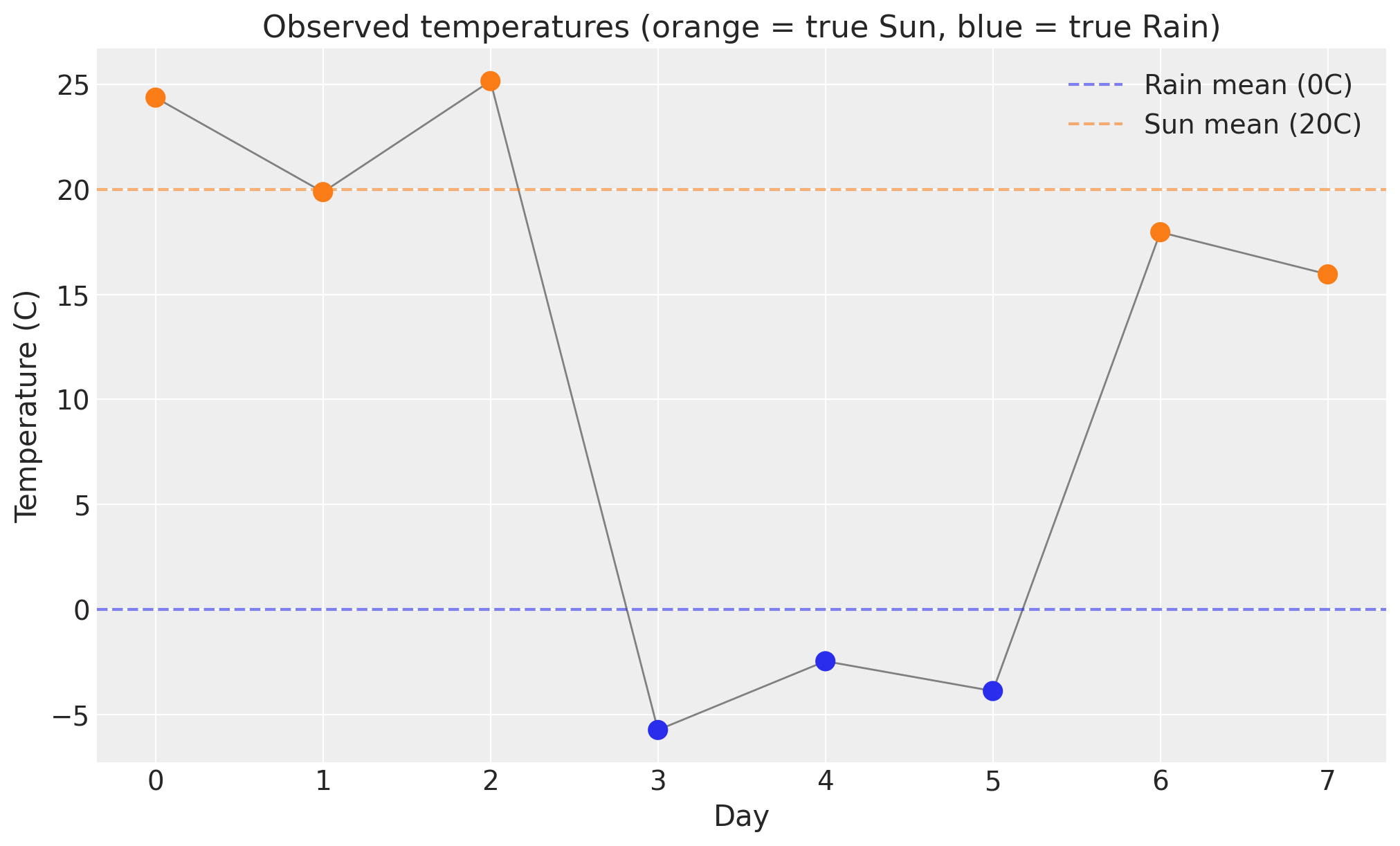

obs_temp.round(2)

Sampling: [sunny_day, temp]

array([24.38, 19.88, 25.16, -5.74, -2.47, -3.88, 17.97, 15.96])

Let’s plot the data.

fig, ax = plt.subplots()

point_colors = np.where(true_sunny_day == 1, "C1", "C0")

ax.plot(days, obs_temp, color="gray", lw=1, zorder=2)

ax.scatter(days, obs_temp, c=point_colors, s=90, zorder=3)

ax.axhline(0, ls="--", color="C0", alpha=0.6, label="Rain mean (0C)")

ax.axhline(20, ls="--", color="C1", alpha=0.6, label="Sun mean (20C)")

ax.legend()

ax.set(

xlabel="Day",

ylabel="Temperature (C)",

title="Observed temperatures (orange = true Sun, blue = true Rain)",

);

The model#

We reuse the same generative model for inference; the only change is that the temperatures are now observed. pm.observe takes the generative model and conditions it on the drawn obs_temp, so we never rewrite the model a second time.

The model places a weakly informative prior on the observation noise, a uniform prior on the first day’s weather, and a DiscreteMarkovChain prior on the sequence of hidden states. The likelihood ties each day’s temperature to its hidden state through a mean of state * 20 degrees.

The transition matrix P is known and fixed here, so we can focus on the marginalize and recover mechanics. In a real application P would typically be given its own Dirichlet prior.

# Reuse the generative model, conditioning on the temperatures we drew above.

model = pm.observe(generative_model, {"temp": obs_temp})

pm.model_to_graphviz(model)

How marginalization works#

Write \(x_{1:n}\) for the hidden states and \(y_{1:n}\) for the temperatures. The HMM factorizes the joint distribution into an initial state, a product of transitions, and a product of emissions:

To sample the continuous parameter \(\sigma\) with NUTS we need the marginal likelihood \(p(y_{1:n} \mid \sigma)\), which sums the joint over every possible state path. Enumerating all \(k^n\) paths is infeasible, but the forward algorithm computes the sum in linear time by carrying forward a vector of partial sums \(\alpha_t(i) = p(y_{1:t}, x_t = i \mid \sigma)\):

The evidence is then \(p(y_{1:n} \mid \sigma) = \sum_i \alpha_n(i)\).

marginal_model = marginalize(model, ["sunny_day"])

pm.model_to_graphviz(marginal_model)

The hidden chain is gone from the graph: only the continuous sigma and the observed temp remain. This is the model NUTS actually samples.

idata = pm.sample(model=marginal_model, target_accept=0.85, random_seed=rng)

Initializing NUTS using jitter+adapt_diag...

Multiprocess sampling (4 chains in 4 jobs)

NUTS: [sigma]

/Users/juanitorduz/Documents/pymc-examples/.venv/lib/python3.14/site-packages/rich/live.py:260: UserWarning:

install "ipywidgets" for Jupyter support

warnings.warn('install "ipywidgets" for Jupyter support')

Sampling 4 chains for 1_000 tune and 1_000 draw iterations (4_000 + 4_000 draws total) took 0 seconds.

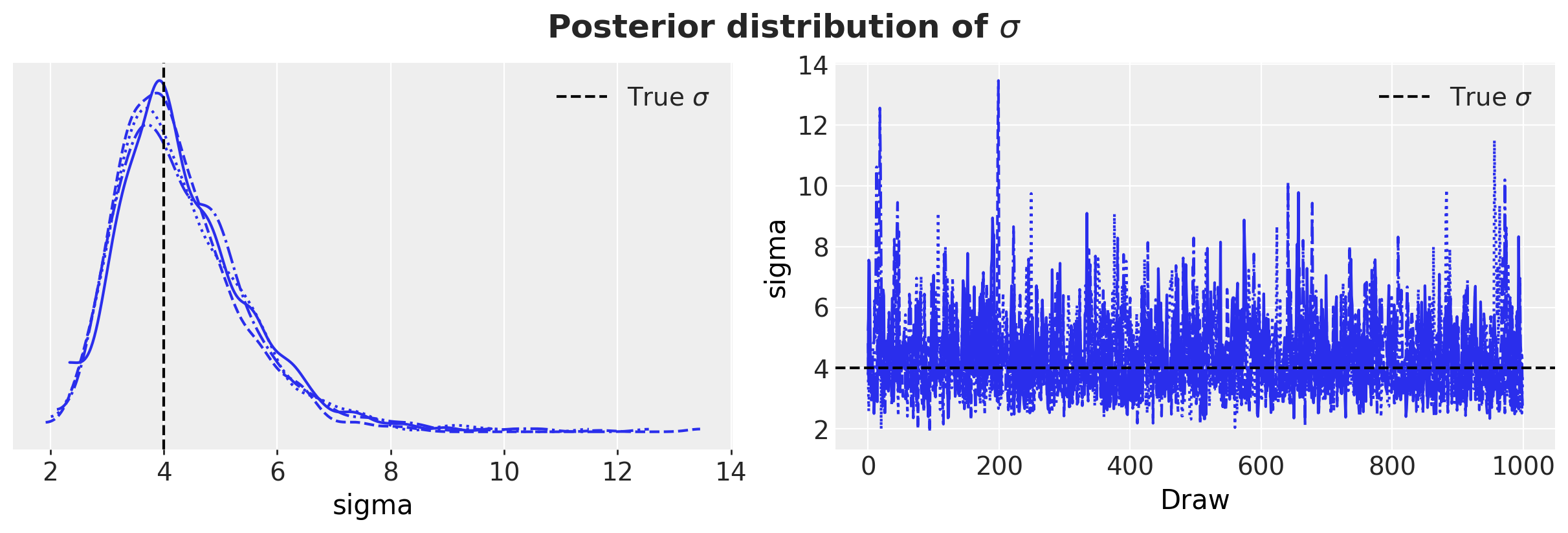

pc = az.plot_trace_dist(idata, var_names=["sigma"], figure_kwargs={"figsize": (12, 4)})

fig = pc.viz["figure"].values.item()

axes = fig.axes

axes[0].axvline(true_sigma, color="k", ls="--", label=r"True $\sigma$")

axes[0].legend(loc="upper right")

axes[1].axhline(true_sigma, color="k", ls="--", label=r"True $\sigma$")

axes[1].legend(loc="upper right")

fig.suptitle(r"Posterior distribution of $\sigma$", fontsize=18, fontweight="bold");

The posterior for sigma is smooth and well behaved because the discrete states are no longer part of the sampled space. The value used to simulate the data was 4.0.

How recovery works#

Marginalizing removed the hidden states, but the states are usually what we actually care about. We want the smoothing posterior \(p(x_t \mid y_{1:n}, \sigma)\), the probability of each hidden state given all of the data and the sampled parameters.

The forward pass above gives \(\alpha_t\). A backward pass gives \(\beta_t(i) = p(y_{t+1:n} \mid x_t = i, \sigma)\), and combining the two yields the per-step smoothing posterior. Crucially, the full conditional \(p(x_{1:n} \mid y_{1:n}, \sigma)\) is itself a Markov chain, but one whose transition matrices change from step to step. This is why time-varying transitions matter: the recovered chain is time-inhomogeneous even when the original chain was homogeneous.

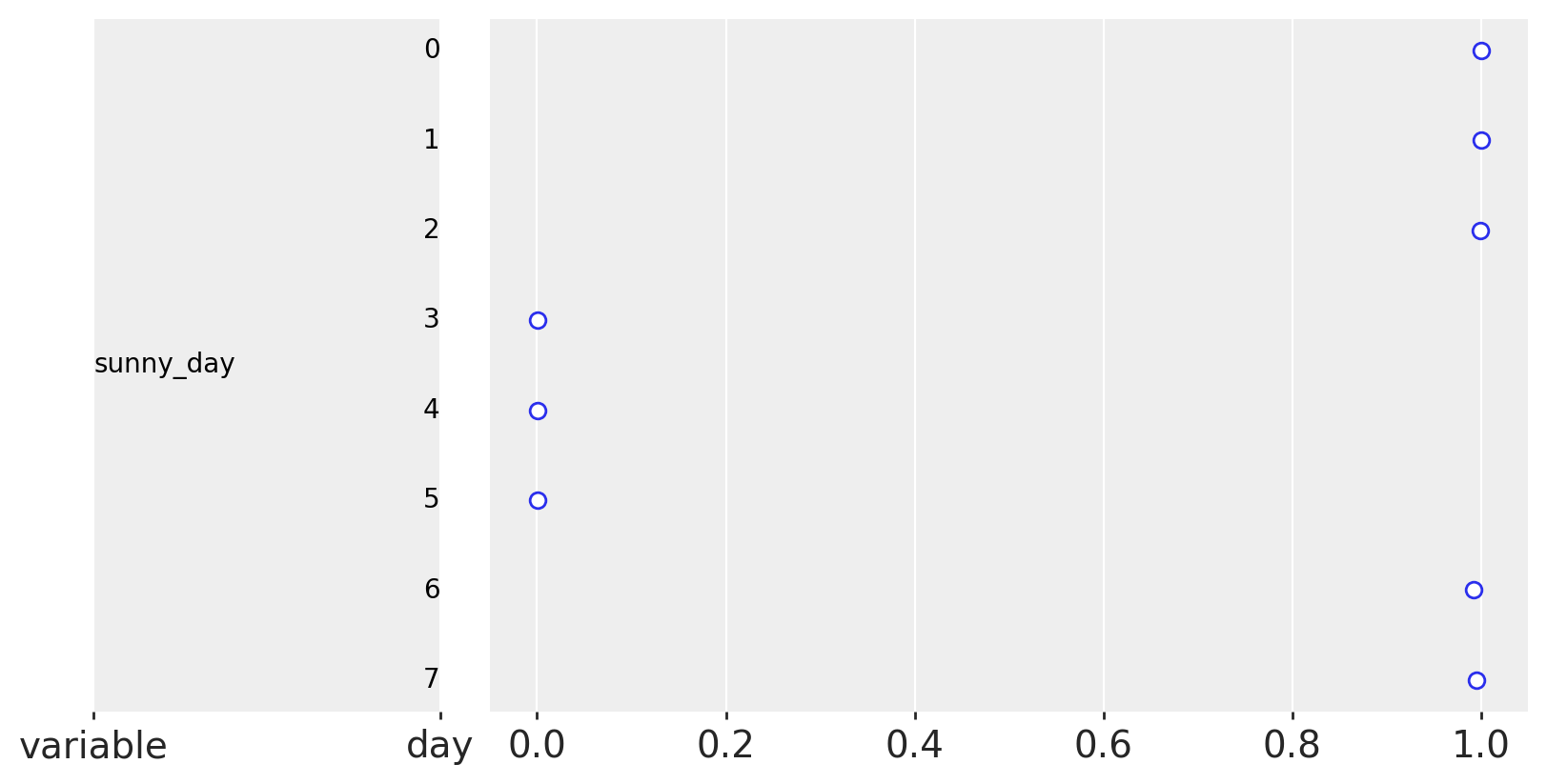

recover(idata, model=marginal_model, random_seed=rng)

p_sun = idata.posterior["sunny_day"].mean(("chain", "draw")).values

print("true Sun: ", true_sunny_day.tolist())

print("recovered P(Sun) per day: ", [float(round(p, 2)) for p in p_sun])

Sampling: [sunny_day]

true Sun: [1, 1, 1, 0, 0, 0, 1, 1]

recovered P(Sun) per day: [1.0, 1.0, 1.0, 0.0, 0.0, 0.0, 0.99, 1.0]

az.plot_forest(idata, var_names=["sunny_day"], combined=True, figure_kwargs={"figsize": (8, 4)});

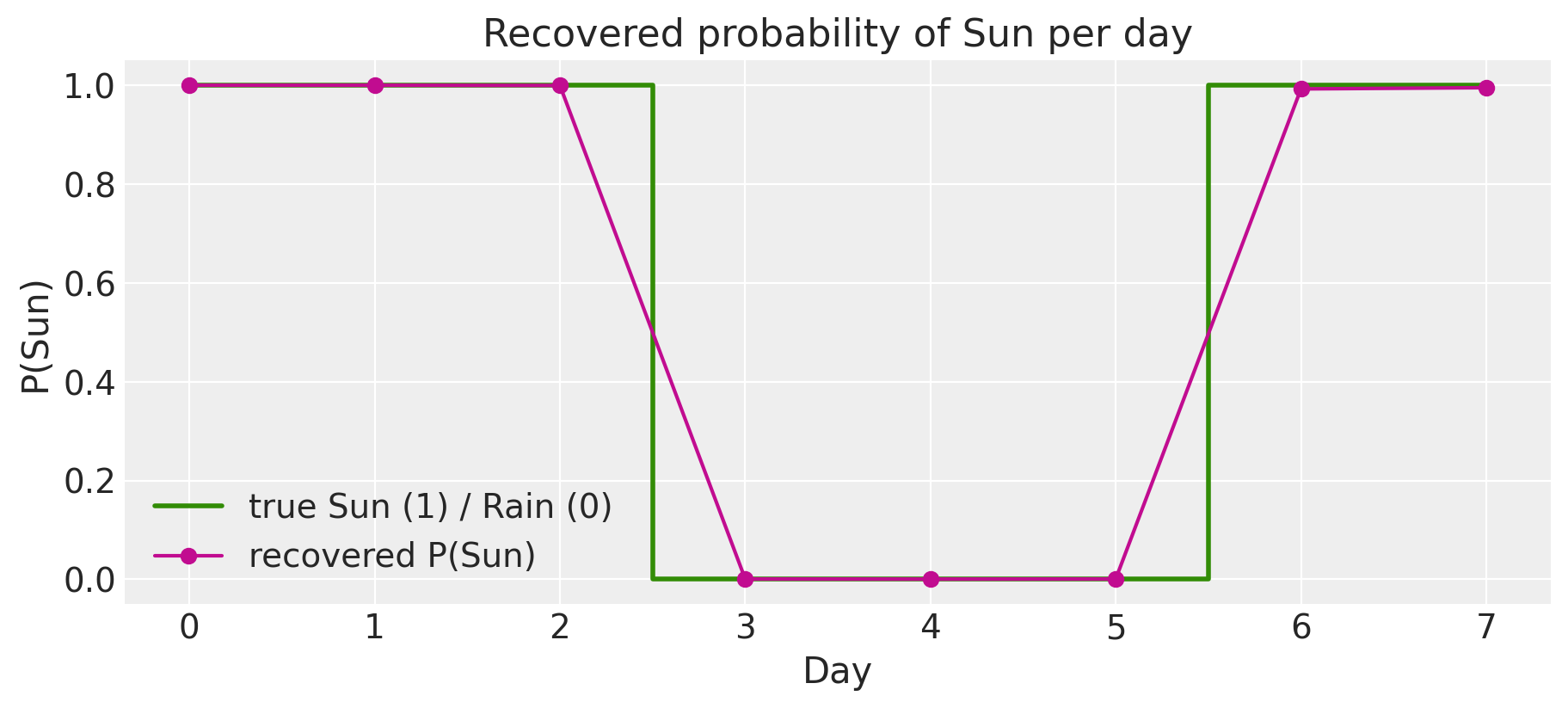

We can plot the recovered probabilities of sun per day.

fig, ax = plt.subplots(figsize=(9, 4))

ax.step(days, true_sunny_day, where="mid", color="C2", lw=2, label="true Sun (1) / Rain (0)")

ax.plot(days, p_sun, "o-", color="C3", label="recovered P(Sun)")

ax.legend()

ax.set(

xlabel="Day",

ylabel="P(Sun)",

ylim=(-0.05, 1.05),

title="Recovered probability of Sun per day",

);

The recovered probabilities snap close to the true path: the model is confident, and correct, about which days were sunny, even though it only ever saw noisy temperatures.

If you need the conditional distribution as a model object rather than posterior draws, conditional gives it to you directly. The recovered sunny_day is now a free random variable whose distribution is the conditional posterior.

cond_model = conditional(marginal_model)

cond_model.free_RVs

[sigma, sunny_day]

Time-varying transitions: a change in the weather regime#

So far the weather was equally sticky on every day: a single transition matrix P governed all of the days. Real weather is not like that. A settled high-pressure spell can hold the same conditions for a week, and then a front arrives and the weather turns unsettled, flipping between sun and rain from one day to the next.

We can capture this by letting the transition matrix change over time. The time_varying_P=True flag lets P carry one transition matrix per step, with shape (steps, k, k) for a single chain (or (*batch, steps, k, k) with batch dimensions), where steps is the number of transitions, one fewer than the number of days.

We continue the weather story over a longer window. The first stretch is a stable, sticky spell; then a front arrives at changepoint and the weather becomes unsettled, close to a coin flip each day.

n_season = 14

days_season = np.arange(n_season)

changepoint = 7 # a weather front arrives, splitting the window into two regimes

# Two transition regimes for the hidden weather.

P_stable = np.array([[0.95, 0.05], [0.05, 0.95]]) # settled: weather persists

P_unsettled = np.array([[0.5, 0.5], [0.5, 0.5]]) # stormy: sun and rain flip freely

# One transition matrix per step: stable before the front, unsettled after.

P_time = np.stack([P_stable] * changepoint + [P_unsettled] * (n_season - 1 - changepoint))

P_time.shape # (steps, k, k) with steps = n_season - 1

(13, 2, 2)

# The same generative model as before, now with a time-varying transition matrix.

with pm.Model(coords={"day": days_season}) as season_generative_model:

sigma = pm.HalfNormal("sigma", 5.0)

init = pm.Categorical.dist(p=[0.5, 0.5])

sunny_day = DiscreteMarkovChain(

"sunny_day", P=P_time, init_dist=init, time_varying_P=True, dims="day"

)

pm.Normal("temp", mu=sunny_day * 20.0, sigma=sigma, dims="day")

# A single prior draw of the weather: long runs during the settled spell, then

# rapid switching once the front arrives. The noise is clamped to true_sigma.

season_prior_draw = pm.sample_prior_predictive(

model=pm.do(season_generative_model, {"sigma": true_sigma}),

draws=1,

var_names=["sunny_day", "temp"],

random_seed=23,

)

true_sunny_day_season = season_prior_draw.prior["sunny_day"].sel(chain=0, draw=0).to_numpy()

obs_temp_season = season_prior_draw.prior["temp"].sel(chain=0, draw=0).to_numpy()

true_sunny_day_season.tolist()

Sampling: [sunny_day, temp]

[1, 1, 1, 0, 0, 0, 0, 0, 1, 1, 0, 1, 0, 0]

The single prior draw above gives us a known weather sequence that spans both regimes together with its noisy thermometer readings. We condition on those readings with pm.observe and then marginalize, sample, and recover exactly as in the first example. Nothing about the workflow changes; only P is now time-varying.

# Reuse the generative model, conditioning on the temperatures drawn above.

season_model = pm.observe(season_generative_model, {"temp": obs_temp_season})

pm.model_to_graphviz(season_model)

We now marginalize and sample.

season_marginal = marginalize(season_model, ["sunny_day"])

season_idata = pm.sample(model=season_marginal, target_accept=0.85, random_seed=rng)

recover(season_idata, model=season_marginal, random_seed=rng)

p_sun_season = season_idata.posterior["sunny_day"].mean(("chain", "draw")).values

print("true Sun: ", true_sunny_day_season.tolist())

print("recovered P(Sun) per day: ", [float(round(p, 2)) for p in p_sun_season])

Initializing NUTS using jitter+adapt_diag...

Multiprocess sampling (4 chains in 4 jobs)

NUTS: [sigma]

/Users/juanitorduz/Documents/pymc-examples/.venv/lib/python3.14/site-packages/rich/live.py:260: UserWarning:

install "ipywidgets" for Jupyter support

warnings.warn('install "ipywidgets" for Jupyter support')

Sampling 4 chains for 1_000 tune and 1_000 draw iterations (4_000 + 4_000 draws total) took 0 seconds.

Sampling: [sunny_day]

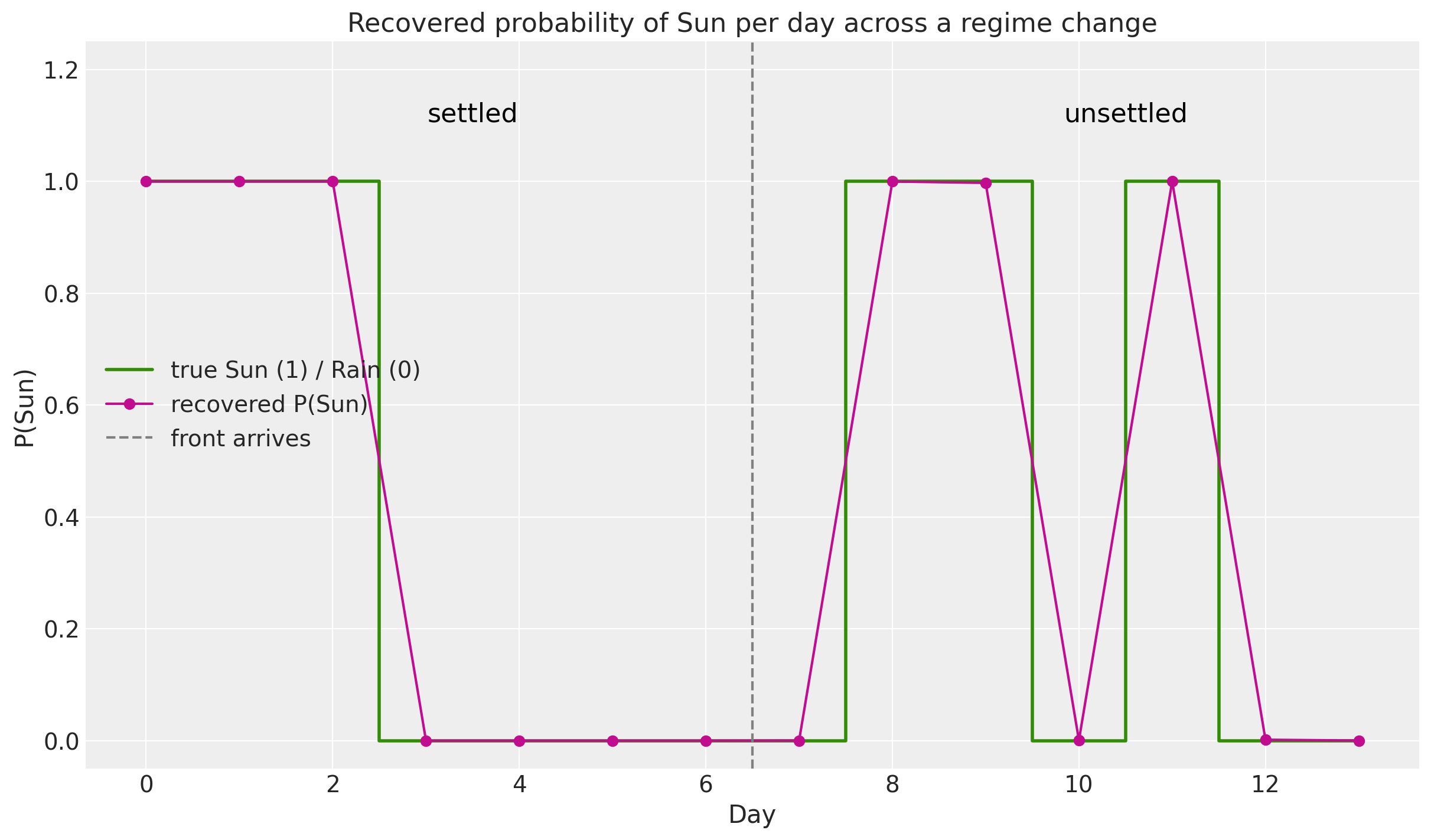

true Sun: [1, 1, 1, 0, 0, 0, 0, 0, 1, 1, 0, 1, 0, 0]

recovered P(Sun) per day: [1.0, 1.0, 1.0, 0.0, 0.0, 0.0, 0.0, 0.0, 1.0, 1.0, 0.0, 1.0, 0.0, 0.0]

Let’s plot the recovered probabilities of sun per day.

fig, ax = plt.subplots(figsize=(12, 7))

ax.step(

days_season,

true_sunny_day_season,

where="mid",

color="C2",

lw=2,

label="true Sun (1) / Rain (0)",

)

ax.plot(days_season, p_sun_season, "o-", color="C3", label="recovered P(Sun)")

ax.axvline(changepoint - 0.5, ls="--", color="gray", label="front arrives")

ax.text(changepoint / 2, 1.12, "settled", size=16, ha="center", va="center", color="black")

ax.text(

(changepoint + n_season) / 2,

1.12,

"unsettled",

size=16,

ha="center",

va="center",

color="black",

)

ax.legend(loc="center left")

ax.set(

xlabel="Day",

ylabel="P(Sun)",

ylim=(-0.05, 1.25),

title="Recovered probability of Sun per day across a regime change",

);

Recovery works identically with time-varying transitions: recover does not care whether P was shared across days or changed from day to day. The recovered probabilities stay sharp across both regimes because the thermometer strongly identifies each day on its own. In the settled spell the sticky transitions reinforce the emissions, while in the unsettled stretch the transitions carry little information, so the recovered states lean almost entirely on the temperatures.

Summary#

We inferred a hidden weather sequence from noisy temperatures using three steps:

Build the model with a

DiscreteMarkovChainprior over the hidden states.marginalizethe chain so NUTS samples only the continuous parameters, using the forward algorithm under the hood.recoverthe hidden states from their exact conditional posterior, which is itself a time-inhomogeneousDiscreteMarkovChain.

Authors#

Authored by Juan Orduz and Ricardo Vieira in July 2026

Watermark#

%load_ext watermark

%watermark -n -u -v -iv -w -p pytensor

Last updated: Tue, 07 Jul 2026

Python implementation: CPython

Python version : 3.14.2

IPython version : 9.15.0

pytensor: 3.0.7

arviz : 1.2.0

matplotlib : 3.10.9

numpy : 2.4.6

pymc : 6.0.1

pymc_extras: 0.12.2.dev12+g1fdbf6ffe

Watermark: 2.6.0

License notice#

All the notebooks in this example gallery are provided under the MIT License which allows modification, and redistribution for any use provided the copyright and license notices are preserved.

Citing PyMC examples#

To cite this notebook, use the DOI provided by Zenodo for the pymc-examples repository.

Important

Many notebooks are adapted from other sources: blogs, books… In such cases you should cite the original source as well.

Also remember to cite the relevant libraries used by your code.

Here is an citation template in bibtex:

@incollection{citekey,

author = "<notebook authors, see above>",

title = "<notebook title>",

editor = "PyMC Team",

booktitle = "PyMC examples",

doi = "10.5281/zenodo.5654871"

}

which once rendered could look like: