Multivariate Gaussian Random Walk¶

import arviz as az

import matplotlib.pyplot as plt

import numpy as np

import pymc3 as pm

import theano

from scipy.linalg import cholesky

%matplotlib inline

RANDOM_SEED = 8927

rng = np.random.default_rng(RANDOM_SEED)

az.style.use("arviz-darkgrid")

This notebook shows how to fit a correlated time series using multivariate Gaussian random walks (GRWs). In particular, we perform a Bayesian regression of the time series data against a model dependent on GRWs.

We generate data as the 3-dimensional time series

where

\(i\mapsto\alpha_{i}\) and \(i\mapsto\beta_{i}\), \(i\in\{0,1,2,3,4\}\), are two 3-dimensional Gaussian random walks for two correlation matrices \(\Sigma_\alpha\) and \(\Sigma_\beta\),

we define the index $\( i[t]= j\quad\text{for}\quad t = 60j,60j+1,...,60j+59, \quad\text{and}\quad j = 0,1,2,3,4, \)$

\(*\) means that we multiply the \(j\)-th column of the \(3\times300\) matrix with the \(j\)-th entry of the vector for each \(j=0,1,...,299\), and

\(\xi_{\mathbf t}\) is a \(3\times300\) matrix with iid normal entries \(N(0,\sigma^2)\).

So the series \(\mathbf y\) changes due to the GRW \(\alpha\) in five occasions, namely steps \(0,60,120,180,240\). Meanwhile \(\mathbf y\) changes at steps \(1,60,120,180,240\) due to the increments of the GRW \(\beta\) and at every step due to the weighting of \(\beta\) with \(\mathbf t/300\). Intuitively, we have a noisy (\(\xi\)) system that is shocked five times over a period of 300 steps, but the impact of the \(\beta\) shocks gradually becomes more significant at every step.

Data generation¶

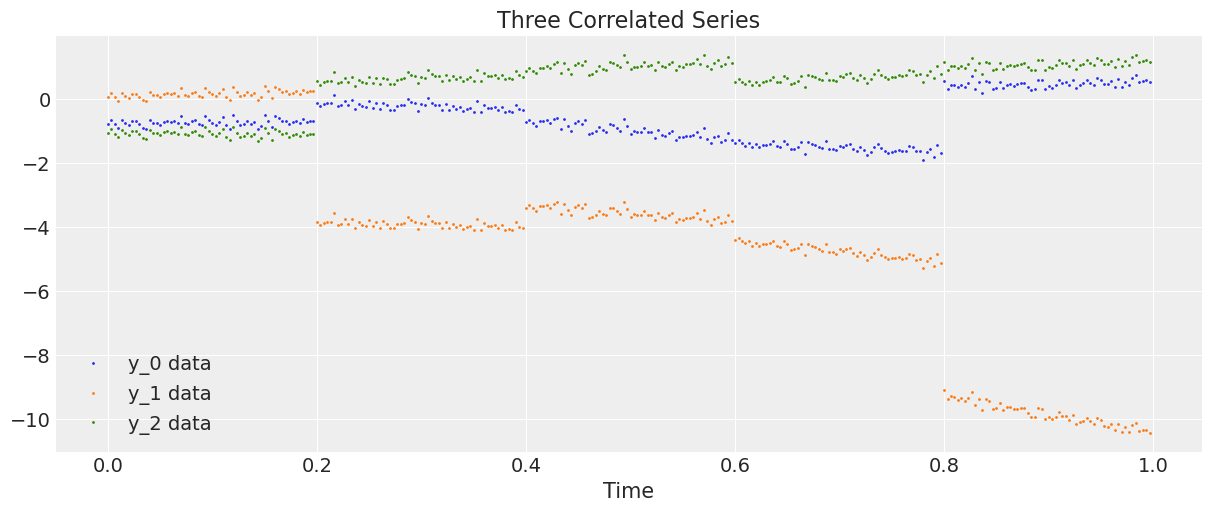

Let’s generate and plot the data.

D = 3 # Dimension of random walks

N = 300 # Number of steps

sections = 5 # Number of sections

period = N / sections # Number steps in each section

Sigma_alpha = rng.standard_normal((D, D))

Sigma_alpha = Sigma_alpha.T.dot(Sigma_alpha) # Construct covariance matrix for alpha

L_alpha = cholesky(Sigma_alpha, lower=True) # Obtain its Cholesky decomposition

Sigma_beta = rng.standard_normal((D, D))

Sigma_beta = Sigma_beta.T.dot(Sigma_beta) # Construct covariance matrix for beta

L_beta = cholesky(Sigma_beta, lower=True) # Obtain its Cholesky decomposition

# Gaussian random walks:

alpha = np.cumsum(L_alpha.dot(rng.standard_normal((D, sections))), axis=1).T

beta = np.cumsum(L_beta.dot(rng.standard_normal((D, sections))), axis=1).T

t = np.arange(N)[:, None] / N

alpha = np.repeat(alpha, period, axis=0)

beta = np.repeat(beta, period, axis=0)

# Correlated series

sigma = 0.1

y = alpha + beta * t + sigma * rng.standard_normal((N, 1))

# Plot the correlated series

plt.figure(figsize=(12, 5))

plt.plot(t, y, ".", markersize=2, label=("y_0 data", "y_1 data", "y_2 data"))

plt.title("Three Correlated Series")

plt.xlabel("Time")

plt.legend()

plt.show();

Model¶

First we introduce a scaling class to rescale our data and the time parameter before the sampling and then rescale the predictions to match the unscaled data.

class Scaler:

def __init__(self):

mean_ = None

std_ = None

def transform(self, x):

return (x - self.mean_) / self.std_

def fit_transform(self, x):

self.mean_ = x.mean(axis=0)

self.std_ = x.std(axis=0)

return self.transform(x)

def inverse_transform(self, x):

return x * self.std_ + self.mean_

We now construct the regression model in (1) imposing priors on the GRWs \(\alpha\) and \(\beta\), on the standard deviation \(\sigma\) and hyperpriors on the Cholesky matrices. We use the LKJ prior [Lewandowski et al., 2009] for the Cholesky matrices (see this link for the documentation and also the PyMC notebook LKJ Cholesky Covariance Priors for Multivariate Normal Models for some usage examples.)

def inference(t, y, sections, n_samples=100):

N, D = y.shape

# Standardies y and t

y_scaler = Scaler()

t_scaler = Scaler()

y = y_scaler.fit_transform(y)

t = t_scaler.fit_transform(t)

# Create a section index

t_section = np.repeat(np.arange(sections), N / sections)

# Create theano equivalent

t_t = theano.shared(np.repeat(t, D, axis=1))

y_t = theano.shared(y)

t_section_t = theano.shared(t_section)

coords = {"y_": ["y_0", "y_1", "y_2"], "steps": np.arange(N)}

with pm.Model(coords=coords) as model:

# Hyperpriors on Cholesky matrices

packed_L_alpha = pm.LKJCholeskyCov(

"packed_L_alpha", n=D, eta=2.0, sd_dist=pm.HalfCauchy.dist(2.5)

)

L_alpha = pm.expand_packed_triangular(D, packed_L_alpha)

packed_L_beta = pm.LKJCholeskyCov(

"packed_L_beta", n=D, eta=2.0, sd_dist=pm.HalfCauchy.dist(2.5)

)

L_beta = pm.expand_packed_triangular(D, packed_L_beta)

# Priors on Gaussian random walks

alpha = pm.MvGaussianRandomWalk("alpha", shape=(sections, D), chol=L_alpha)

beta = pm.MvGaussianRandomWalk("beta", shape=(sections, D), chol=L_beta)

# Deterministic construction of the correlated random walk

alpha_r = alpha[t_section_t]

beta_r = beta[t_section_t]

regression = alpha_r + beta_r * t_t

# Prior on noise ξ

sigma = pm.HalfNormal("sigma", 1.0)

# Likelihood

likelihood = pm.Normal("y", mu=regression, sigma=sigma, observed=y_t, dims=("steps", "y_"))

# MCMC sampling

trace = pm.sample(n_samples, cores=4, return_inferencedata=True)

# Posterior predictive sampling

trace.extend(az.from_pymc3(posterior_predictive=pm.sample_posterior_predictive(trace)))

return trace, y_scaler, t_scaler, t_section

Inference¶

We now sample from our model and we return the trace, the scaling functions for space and time and the scaled time index.

trace, y_scaler, t_scaler, t_section = inference(t, y, sections)

Only 100 samples in chain.

Auto-assigning NUTS sampler...

Initializing NUTS using jitter+adapt_diag...

Multiprocess sampling (4 chains in 4 jobs)

NUTS: [sigma, beta, alpha, packed_L_beta, packed_L_alpha]

Sampling 4 chains for 1_000 tune and 100 draw iterations (4_000 + 400 draws total) took 1836 seconds.

0, dim: steps, 300 =? 300

1, dim: y_, 3 =? 3

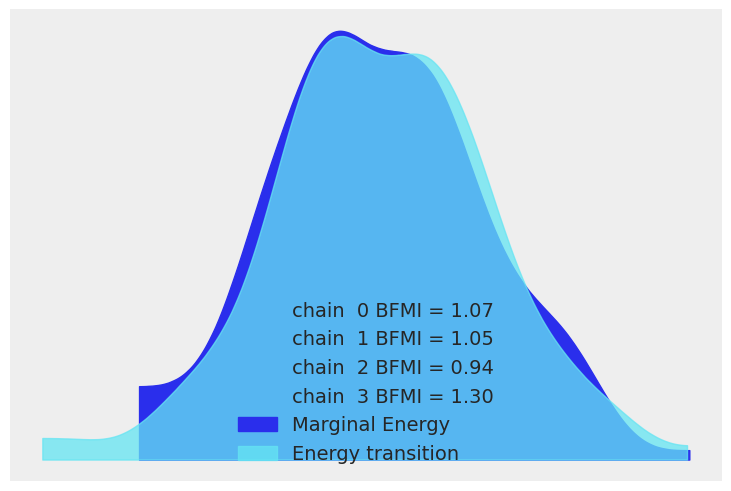

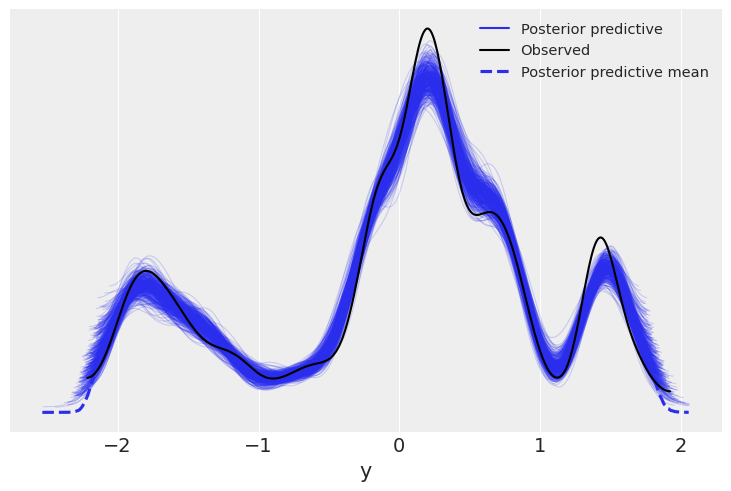

We now display the energy plot using arviz.plot_energy() for a visual check for the model’s convergence. Then, using arviz.plot_ppc(), we plot the distribution of the posterior predictive samples against the observed data \(\mathbf y\). This plot provides a general idea of the accuracy of the model (note that the values of \(\mathbf y\) actually correspond to the scaled version of \(\mathbf y\)).

az.plot_energy(trace)

az.plot_ppc(trace);

Posterior visualisation¶

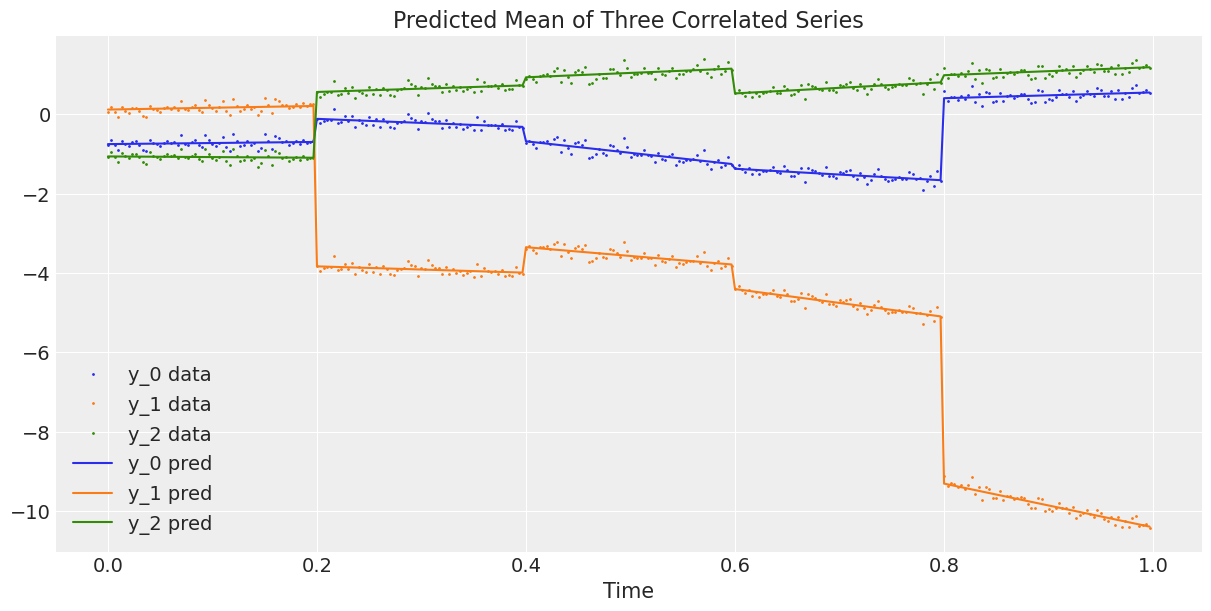

The graphs above look good. Now we plot the observed 3-dimensional series against the average predicted 3-dimensional series, or in other words, we plot the data against the estimated regression curve from the model (1).

# Compute the predicted mean of the multivariate GRWs

alpha_mean = trace.posterior["alpha"].mean(dim=("chain", "draw"))

beta_mean = trace.posterior["beta"].mean(dim=("chain", "draw"))

# Compute the predicted mean of the correlated series

y_pred = y_scaler.inverse_transform(

alpha_mean[t_section].values + beta_mean[t_section].values * t_scaler.transform(t)

)

# Plot the predicted mean

fig, ax = plt.subplots(1, 1, figsize=(12, 6))

ax.plot(t, y, ".", markersize=2, label=("y_0 data", "y_1 data", "y_2 data"))

plt.gca().set_prop_cycle(None)

ax.plot(t, y_pred, label=("y_0 pred", "y_1 pred", "y_2 pred"))

ax.set_xlabel("Time")

ax.legend()

ax.set_title("Predicted Mean of Three Correlated Series");

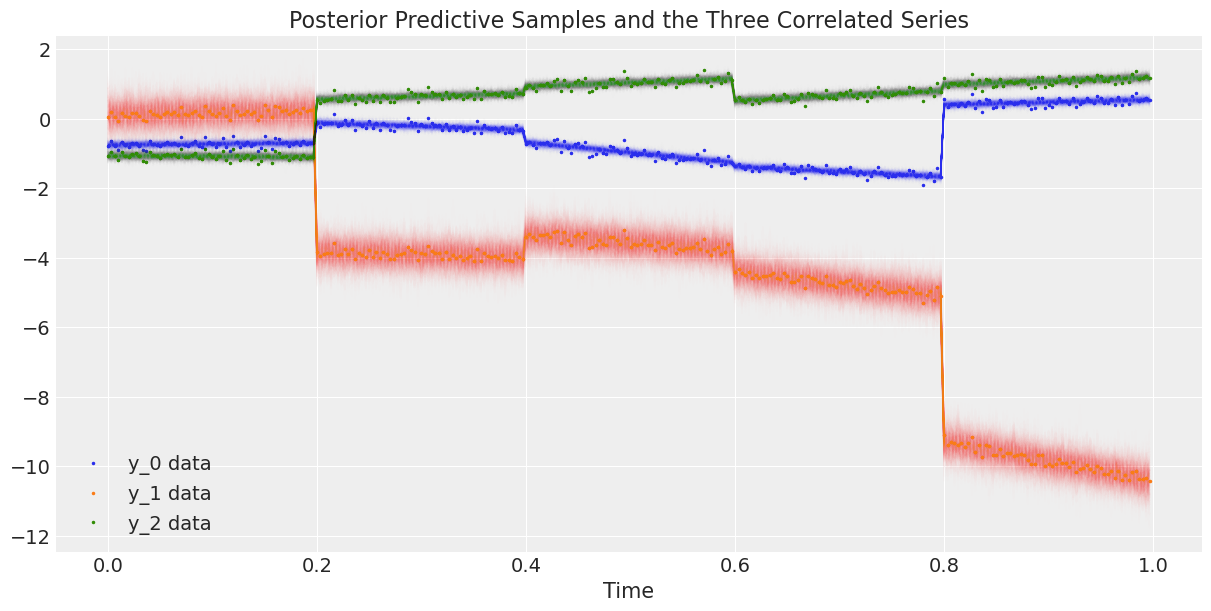

Finally, we plot the data against the posterior predictive samples.

# Rescale the posterior predictive samples

ppc_y = y_scaler.inverse_transform(trace.posterior_predictive["y"].mean("chain"))

fig, ax = plt.subplots(1, 1, figsize=(12, 6))

# Plot the data

ax.plot(t, y, ".", markersize=3, label=("y_0 data", "y_1 data", "y_2 data"))

# Plot the posterior predictive samples

ax.plot(t, ppc_y.sel(y_="y_0").T, color="C0", alpha=0.003)

ax.plot(t, ppc_y.sel(y_="y_1").T, color="C1", alpha=0.003)

ax.plot(t, ppc_y.sel(y_="y_2").T, color="C2", alpha=0.003)

ax.set_xlabel("Time")

ax.legend()

ax.set_title("Posterior Predictive Samples and the Three Correlated Series");

References¶

- 1

Daniel Lewandowski, Dorota Kurowicka, and Harry Joe. Generating random correlation matrices based on vines and extended onion method. Journal of multivariate analysis, 100(9):1989–2001, 2009.

Watermark¶

%load_ext watermark

%watermark -n -u -v -iv -w -p theano,xarray

Last updated: Sat Sep 25 2021

Python implementation: CPython

Python version : 3.9.6

IPython version : 7.26.0

theano: 1.0.5

xarray: 0.19.0

arviz : 0.11.2

numpy : 1.21.1

matplotlib: 3.4.2

theano : 1.0.5

pymc3 : 3.11.2

Watermark: 2.2.0

- PyMC Contributors . "Multivariate Gaussian Random Walk". In: PyMC Examples. Ed. by PyMC Team. DOI: 10.5281/zenodo.5832070